Large-scale solar essential to solving Africa’s energy crisis

Africa’s rapidly growing demand for power cannot be met by traditional sources alone. Solar PV is affordable, available and scalable.

Scatec Solar plant under construction in Kalkbult, South Africa (photo: scatecsolar.com)

The 48 countries of sub-Saharan Africa, excluding South Africa, represent 10 percent of the world’s population, but consume less electricity than Poland. The region’s electrification rate is the lowest in the world, at below 30 percent.

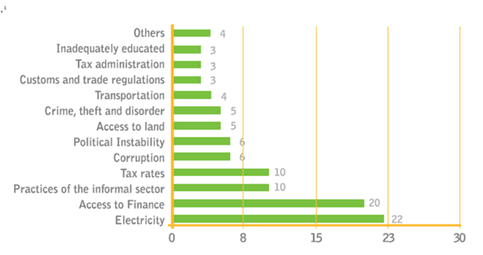

Access to reliable, affordable electricity is perceived by entrepreneurs and businesses as the most important obstacle to doing business in sub-Saharan Africa according to at a 2012 survey by the African Development Bank.

Source: Heinrich Böll Stiftung, World Future Council: Powering Africa through Feed-in-Tariffs: Advancing renewable energy to meet the continent's electricity needs.

Despite the limited capacity installed, sub-Saharan Africa suffers from excessively high costs of power generation. This can partly be explained by the role played by high-cost diesel- and fuel-generated power in meeting the fast-rising demand growth. There is a broad understanding among stakeholders that Africa’s rapidly growing demand for power cannot be met by traditional sources alone:

Hydropower still holds a large potential for growth, but projects seem increasingly to suffer from controversy and delays raised by social and environmental issues. In addition, prolonged droughts and more extreme weather patterns will negatively affect the reliability of hydropower. Governments should therefore seek to extract more value from the limited high-value hydro resources as dispatchable power supply, in combination with the unlimited but non-dispatchable solar and wind resources.

In several parts of Africa, Natural Gas is set to become the most important source of power generation. However, gas is neither cheap nor abundant. Experience shows that the costs of bringing the gas to market are usually underestimated in the planning phase. With the extension of pipelines and LNG export terminals, even gas customers in gas-producing countries will face increased competition from energy-hungry customers in neighbouring countries and markets overseas. On the other hand, by replacing gas-power with solar power at daytime, gas-producing countries can increase export revenues and prolong the lifetime of the limited gas resources. This has for example been the motivation for countries like Saudi Arabia and the UAE to embark upon ambitious solar energy programs recently.

A number of new coal generation plants are in the planning phase in different parts of Africa. However, the projects are slow to materialise, and cost estimates are regularly adjusted upwards. The projects are difficult to finance, not least due to the uncertainty about future costs of fuel and CO.

2

In some African countries energy plans also include nuclear plants. However the challenge of developing, permitting, financing and executing nuclear plants can hardly be underestimated. Given the difficulty for nuclear to break through in the rest of the world, nuclear energy can hardly be seen as a credible option in sub-Saharan Africa the next five to ten years.

Solar PV – affordable, available, scalable

Solar PV is an important answer to Africa’s looming power crisis, not least because it can be implemented in very short time. Example: Scatec’s first project in South Africa, the 75 MW Kalkbult plant currently under construction, will be grid-connected in less than a year from the signing of the PPA. This very point is also highlighted in a recent report from International Renewable Energy Agency (IRENA): "Solar PV also has the advantage that, once the domestic installation market is developed, solar PV installations can be ramped up rapidly to meet policy goals or electricity sector needs, no other power generation technology shares this flexibility" (Renewable Power Generation Costs – Summary for policy makers, 2012).

Solar PV will contribute to more affordable power and enhanced energy security. Solar PV reduces the dependence on imported power and by replacing diesel-generated power it contributes to improved electricity quality (voltage and frequency). Large-scale solar PV can play a critical role in eliminating sub-Saharan Africa’s dependence on imports of costly fossil fuels, as well as developing the countries’ domestic economy and employment.

Benefits of introducing large-scale solar PV:

In a first phase, solar PV is suited to meet on average around 15-20 percent of Africa’s fast-growing electricity consumption. In the medium- and long-term solar PV can play a much larger role in the countries’ energy mix, when combined with:

However, despite the fact that several sub-Sahara countries have introduced targets and incentives for renewables, no country outside South Africa has so far succeeded in introducing substantial volumes of grid-connected solar PV.

Setting the targets

Governments should set political targets for grid-connected solar PV over a time-period. Targets are important signals for developers, investors and equipment suppliers and targets can justify up-front investments.

As highlighted by the Heinrich Böll Stiftung/World Future Council study "Powering Africa through Feed-in-Tariffs" (2012) it is recommended to "establish targets for the short, mid and long term, thus establishing a pathway of how renewables can increasingly substitute fossil and nuclear power generation sources."

However, it is important that the targets are not perceived as long-term caps on the installation of solar PV, and should therefore include the words "at least"(e.g. at least 20 percent penetration by 2020). With growing demand, higher costs of alternatives and falling costs of PV, caps set today can easily prove to be artificially constraining a few years ahead.

Targets can be defined as a certain share of renewables in the overall energy or electricity demand, or can apply to the installed capacity. Targets as share of total electricity demand is preferable as this measure include imports and exclude exports of power.

In many countries, there are discussions on the topic of limiting the size of plants eligible for the defined tariff system. But setting caps per project will in most cases increase the cost per MW installed. The decision to define the right size of each plant should be left to a technical-financial discussion and review between the developer, the grid operator and off-taker. It is important to recognise that for global companies a minimum project size is required to justify the necessary investments in developing, structuring, negotiating, financing, executing, constructing, commissioning and start operating a solar plant in a new market.

In general, 20 MWp should be seen as a minimum project size to justify the costs and other resources required to raise project finance from international sources like IFC and other international development finding associations as well as international commercial banks. The larger the plant, the lower per unit costs of development, asset structuring and financing, procurement, construction and operation and maintenance – and hence also the cost of electricity produced by the plant.

On the other hand, in some countries, PV plants in the size 20-30 MW may simply be too big to accommodate, mainly due to grid constraints. In such cases, utilities may encourage developers to propose multi-site projects, ie. projects that include several medium-sized plants connected to different sub-stations.

Tender or negotiations

The fundamental idea behind a feed-in-tariff is the guarantee that the state utility will buy all the electricity provided to the grid. However, African countries seem to be moving away from European-style feed-in-tariff–regimes for large-scale solar, presumably due to fear of administrative overload and unchecked growth. In practice, it has proved difficult for governments to adjust tariffs at a rate correctly corresponding to declining costs of PV.

This effectively leaves two forms of allocation mechanism:

Many countries are seeking a combination of the two, by organising a pre-qualification tender. The selected pre-qualified independent power producers (IPPs) will then be invited to make proposals and negotiate directly with the off-taker, which most often will be the utility company.

The experience shows that international tenders are very time- and resource-consuming, and can normally only be justified in big markets like for example South Africa, Morocco, Saudi Arabia and India. Compared to direct negotiations, an international tender could in addition end up delaying the award process by anything from six months to one to two years. Furthermore, in most cases developers will not be in position to obtain grants or soft loans for the project if the proposal is part of a bidding process. The result may therefore be that a tender easily can result in higher financing costs and hence higher tariffs compared to a situation where the developer can work with the financing partner as part of the development and negotiating process.

On the other hand, tenders have the advantage of securing competition and transparency. A combination of the two approaches can therefore be envisaged if time allows:

Is solar PV expensive?

The costs of solar PV have fallen radically in the past few years, but in most countries the cost plus reasonable return tariffs offered by Solar IPPs are still higher than the average generation costs in the country. This is not surprising, given that the lion’s share of grid-connected power available today is being supplied by old and amortised hydro and coal plants.

However, the general belief that solar PV is more expensive than the alternatives seems no longer correct:

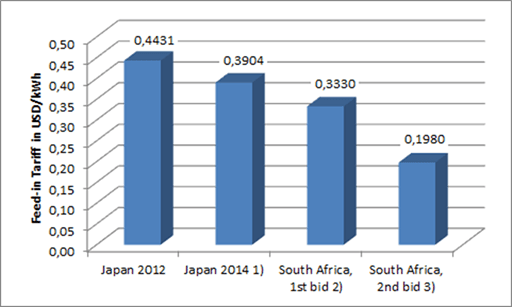

Example: Initial and subsequent tariffs in two new markets.

Whereas the costs of renewables are falling, the costs of alternatives – fossil fuels and nuclear – will continue to rise in the decades to come. This is partly because of higher costs of exploring, extracting, processing and transporting fuels, and partly because the task of building new thermal and nuclear power plants are getting ever more expensive when also considering the full environmental and safety aspects of the projects.

Furthermore, fuel prices are expected to continue to rise. In its latest reference scenario, IEA forecasts that the nominal market prices for crude oil, natural gas (US) and coal will rise by approximately 100 percent, 300 percent and 60 percent respectively from 2011 and 2035. Even in real terms, the prices for crude oil and natural gas (except Asia) are expected to increase significantly in the period.

It should also be noted that, despite the current depression in the carbon markets, most observers expect that some kind of global price or tax on CO2 will come into force in the next five to 10 years, further adding to the price increases above. ExxonMobil for example, forecast that the cost of CO2 will reach US$60 per tonne by 2030.

It is therefore impossible to say whether the cost of solar PV contracted today will be higher or lower than the alternatives coming up in the 20 year contract period. But solar PV appears to be more costly today, because PV typically requires a tariff to be set for the entire PPA period (e.g. 20 years) for the project to attract the requisite financing for the large up-front investment. However, the fuel for the plant is inherently free, whereas the alternatives will be linked to price of fossil fuels for the entire duration of the operational phase as well as the costs of the CO2 emitted in the process.

Nevertheless, the upfront additional costs of PV should be passed on to the electricity consumers. This is done by establishing the purchase obligation for the existing utilities, and allowing these to adjust tariffs accordingly. With a fixed tariff for 20 years, the consumers are – for this minor part of total supply − insured against any negative surprises due to fuel price fluctuations.

Contractual and grid requirements

To succeed, large-scale adoption of renewables must go hand-in-hand with upgrading and development of the electricity grid. What are the lessons learnt by system operators with a longer track-record of integrating wind and solar power?

In a report from 2011, The Global Sustainable Electricity Partnership, a nonprofit organisation whose members include Duke Energy, EDF, RWE, Enel, Eskom, outlines solutions to secure a good integration of renewable energies in the energy system. Although the authors highlight that wind power is much less predictable and therefore much more of a challenge than solar PV, the report provides a few important general messages:

However, it is important not to let the discussion of the required development of the grid block the necessary decisions in the short-term. Africa can benefit from the first stages of affordable, available, and scalable solar PV while at the same time preparing the energy system for a further increased penetration of renewables in the medium– and long-term.