A forecast of the energy transition to 2050

Keeping global warming below 2°C is not likely based on current emission pledges. Investors should consider various scenarios, including scenarios leading to high-end catastrophic changes and low-end scenarios requiring ambitious policies and high transitional risk.

In early September DNV GL launched its Energy Transition Outlook (ETO), a global and regional forecast of the energy transition to 2050.

Do we need another energy outlook?

We have two outlooks from the International Energy Agency, the Energy Technology Perspectives and the World Energy Outlook. Most oil companies produce energy outlooks, including the Statoil Energy Perspectives. The Intergovernmental Panel on Climate Change (IPCC) performs an assessment, every five years or so, on the Mitigation of Climate Change including analysis of emission scenarios. Many more exist.

The DNV GL outlook is a bit different to the others, it is a forecast and not a scenario.

Energy outlooks are generally based onscenarios. Since the future is highly uncertain, scenarios are used to explore the consequences of these future uncertainties. Essentially, scenarios are used to explore how the global energy system may develop under a set of assumed and stylised future worlds.

The DNV GL energy transition outlook is a forecast, a prediction of the future. Essentially, they take a stance on where the world is going.

QUOTE:"Our intention, from the outset, has been to construct what we in DNV GL see as ‘a most likely future’ for energy through to 2050."

QUOTE:"Our intention, from the outset, has been to construct what we in DNV GL see as ‘a most likely future’ for energy through to 2050."

To cut to the chase, the DNV GL energy transition outlook ends with a world that burns enough coal, oil, and gas leading to about 2.5°C at the end of the century.

DNV GL still"strongly supports the Paris Agreement", implying they want the world to be"well below 2°C".

Why would they want to look at an outlook for a 2.5°C world?

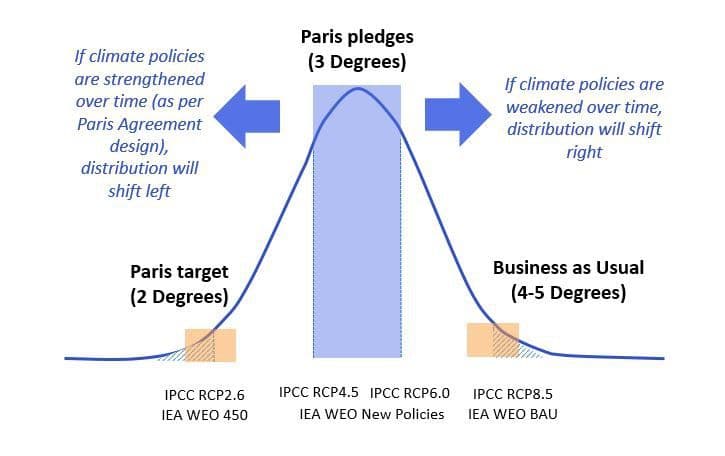

In a risk setting, I would argue it is necessary to know where the world is going. The risk (and opportunity) for incumbents is to deviate from the expected path. To use a common example, if the world moves faster towards climate action, then there is a risk of stranded assets and opportunities in renewable energy technologies.

CICERO Climate Finance has used a similar framing. Financial risk associated with climate impacts or rapid societal transitions lies in the tails of the probability distribution, moving away from where current investments lie, thereby exposing financial and physical assets. The opportunities also lie in the tails, investing early before the transition is made.