Large energy users need more space than rooftops to cover their needs, and have therefore started a new trend: to buy power from dedicated wind and solar plants. The 175 MW Don Rodrigo solar PV plant south of Seville in Spain, developed by the German developer BayWa r.e., is here an example. Falling equipment costs, high solar irradiation, supportive local governments and innovative plant design are all factors explaining the success of Europe’s first subsidy-free utility solar PV plant. The abolition last year of EU import duties on solar modules from China was also helpful. The factor unlocking the investment was the 15 year off-take contract with Statkraft, the Norwegian state-owned clean energy power producer and seller, who will offer the solar power from the plant to corporate customers seeking 100% renewable electricity supply. The plant is now 100% owned by the asset management arm of Munich Re, the giant global reinsurer that is also a leading force in the movement urging the finance industry to take on climate investments.

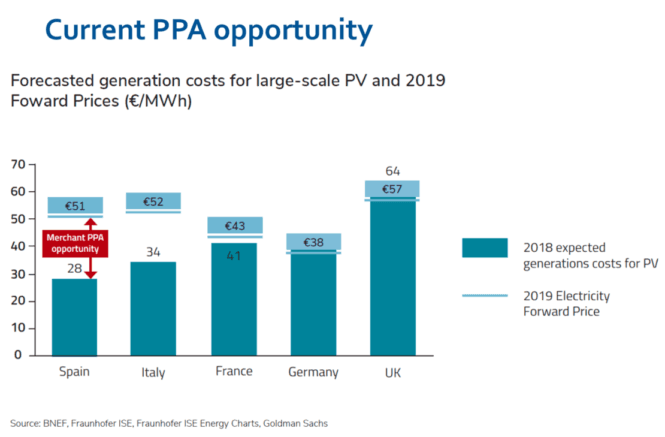

Since the construction of Don Rodrigo started last year, we have seen announcements of several similar large-scale subsidy-free PV projects in other countries, notably in Germany, Portugal, Spain and even the UK. Bloomberg reports that a total of more than 4 GW of unsubsidized solar power purchase agreements (PPAs) had been announced by February 2019.

One example of businesses procuring solar power is IKEA, that has installed 900,000 modules, 154 MWp, on its own roofs, generating 81% of its total power consumption. IKEA intends to use corporate PPAs to become 100% self-sufficient with renewable energy.

Another player to watch is "RE 100", a global club of 155 "green corporations" that has set a target of being powered 100% by renewable energy. The club is recruiting new members in Europe and is also a founding partner behind a new initiative called "RE-Source"; a platform lobbying for frameworks supporting corporate renewable energy sourcing in Europe.

The lesson from the Nordic power market, hitherto the largest large-scale corporate PPAs in Europe, is clear: building an integrated electricity market enabling cross-border long-term power sale contracts is a key enabler for a sustained growth of corporate PPAs.

The third driving force behind Europe’s solar revival is digitisation, strongly enabling energy-smart homes, communities and grids. Solar Power Europe believe 30 million roofs should be equipped with solar panels over the next 10 years and advocate mandatory rules for new buildings, like they have in California and the German town Tübingen.

Utilities are gradually introducing incentives for building an "intelligent grid" that will accommodate a much higher share of renewables, but much more can be done according to the industry. Solar plants can be equipped with advanced power electronics and, gradually, storage capabilities that will render the power networks more reliable. Such upgrading will open up for "on demand" electricity across Europe, also integrating intelligent charging and discharging of electric vehicles connected to the grid. The result will be greatly increased demand for solar power, and also put Europe-based companies in the forefront of innovation.

The new and somewhat surprising interest in "solar fuels" will, when materialized, further add to the emerging boom in utility-scale solar PV. A handful of experienced developers I met at the summit were involved in "power-to-gas" initiatives, targeting to sell hydrogen from solar-powered plants, as that blended with natural gas would serve as fuel in gas-fired power plants.

However, as the cost of solar power falls below $ 0.05/kWh in southern Europe, hydrogen producing companies like NEL claims it can also make a feasible business case for producing hydrogen and transporting it to the pumping station. The projected growth in both electric and hydrogen-driven transport should translate into additional demand for solar power in Europe the coming decades.

But how will a solar growth scenario as outlined here affect jobs and technology innovation in Europe? According to a report by Ernst & Young prepared for Solar Power Europe, reaching 20% market share for solar in 2030 would translate into more than 500,000 new jobs by 2030. Europe will without doubt continue to excel in software, services, installation and fundamental technology, but what about manufacturing? Today, practically all solar cells installed in Europe are imported from China and other Far East countries, and many fear this pattern will be repeated for power electronics, batteries, etc. A question then is whether or not Europe should develop an industrial strategy that also includes some protection for Europe-based manufacturers. When it comes to batteries, initiatives from the EU Commission and recently Germany and Poland have the establishment of manufacturing as objective.

At this point the solar industry is divided between the remaining European manufacturers, companies like Sunpower, Wacker, and SMA plus a number of smaller module manufacturers, and the remaining industry whose main interests are "down-stream" in the value chain. However, the discussions at the summit also revealed a third position with the potential to unite both manufacturers and developers.

The experience from France, who successfully introduced carbon footprint as one of three criteria of selecting solar power bidders, is now being studied with interest at the European level. The current unregulated trade in solar modules has made Europe more and more dependent on imports of products manufactured with energy from polluting coal power plants in inner Mongolia. It could be questioned if this is what Europe wants. The outcome of the debate could be mandatory standards for the modules’ energy efficiency and life-cycle carbon footprint, as part of EU's new Ecodesign Directive for example.

Clearly Europe has the potential, but is it ready to play a leading role in setting the standards for tomorrow's solar-centric energy era?