It is not easy being an oil company with the climate threat hanging over us. How long can Statoil’s strategy be a bet against successful climate policies?

Statoil is a giant in Norwegian terms. The company has 23.000 employees and activities in 36 countries, a stock market value of NOK 417 billion ($55bn, as of Jan. 9, 2015) and a history as Norway’s most important tool in the recovery of petroleum resources on our continental shelf.

Statoil is also a very important player in its role as a customer. The company bought goods and services for a dizzying NOK 127 billion ($17bn) from Norwegian suppliers in 2013. How the company will develop is very important for the future of a large number of Norwegian jobs outside the company’s own operations. Statoil is therefore an industrial motor of great significance for Norway.

We all have an interest in Statoil. Because Statoil is a big company, and because the state owns 67 per cent of the shares, all Norwegian citizens have a right to an opinion on the company’s behaviour and strategy. There is broad agreement that politicians should not micromanage the company. But does that mean that the government and Storting – as representative for the owners – should keep their distance even when it comes to important strategic choices such as whether the company should be investing in renewable energy?

There are no obvious answers to this question, but it is certainly legitimate to debate this and similar issues in the public arena.

At the time of writing, Statoil has just appointed a new CEO, Eldar Sætre, while the oil price has dropped dramatically in the last few months. The short-term challenges facing Sætre are of a significant scope. Costs must be cut.

But where does the company stand in light of climate policies and changes in the energy picture which will have long-term effects? It is the long-term perspective that is discussed in this memo.

What does the climate policy mean and where are the energy markets headed?

Like all the big oil companies, Statoil has assumed that the demand for oil and gas will increase in the decades to come. The essence of this story is that increased population and economic development in emerging markets and developing countries will result in continued growth in demand, even if the OECD countries’ use of oil stagnates.

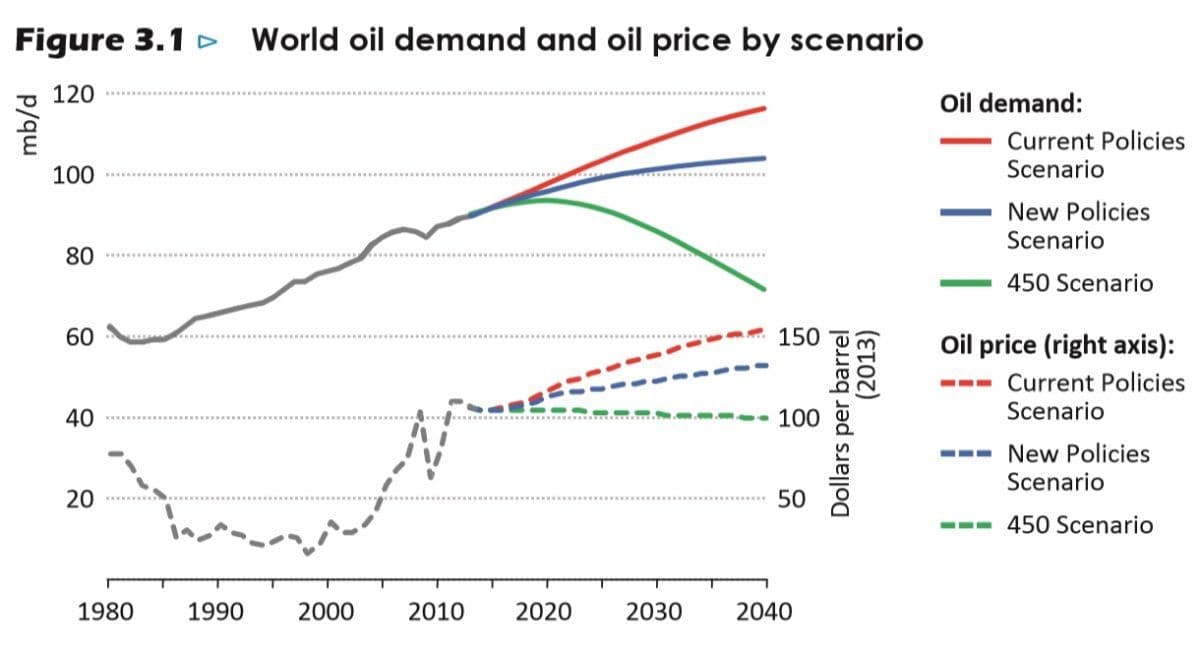

Like the other oil companies, Statoil has prepared forecasts which indicate future demand that will far exceed the oil consumption suggested in the IEA’s two-degree scenario. The oil companies are of the belief that the climate policies will not be successful.

This graph from the IEA’s World Energy Outlook (2014) shows how oil consumption (and prices) might develop in three different climate scenarios: the 450 scenario is the two-degree scenario. The scenarios from the oil companies are broadly in line with the new policy scenario.

The American ExxonMobil is clearer in its wording than Statoil. ExxonMobil is of the opinion that it is "highly unlikely" that the two-degree target will be reached. In a reply to investors who were asking questions about Exxon’s handling of carbon risk towards 2050, the following was stated:

"ExxonMobil believes that although there is always the possibility that government action may impact the company, the scenario where governments restrict hydrocarbon production in a way to reduce GHG emissions 80 percent during the Outlook period is highly unlikely."

For this reason, there is no reason for investors to worry about Exxon’s reserves losing their value.

"In assessing the economic viability of proved reserves, we do not believe a scenario consistent with reducing GHG emissions by 80 percent by 2050, as suggested by the ‘low carbon scenario,’ lies within the ‘reasonably likely to occur’ range of planning assumptions, since we consider the scenario highly unlikely." "We are confident that none of our hydrocarbon reserves are now or will become ‘stranded.’ We believe producing these assets is essential to meeting growing energy demand worldwide, and in preventing consumers – especially those in the least developed and most vulnerable economies – from themselves becoming stranded in the global pursuit of higher living standards and greater economic opportunity."

This is plain speaking. A level of demand for oil and gas in line with the two-degree target, i.e. a successful climate policy, is unlikely, according to Exxon.

In the autumn of 2013, Statoil responded to an enquiry from the American think tank Ceres. Statoil’s statement with regard to carbon risk is fairly similar to Exxon’s recent statement, but places more emphasis on the severity of the climate threat.

Statoil underlines that the company is in favour of climate policy:

"The 450 Scenario of the IEA is based on an assumption of climate policies being implemented globally within the next few years and that global GHG emissions from energy starts to decline before 2020. It is Statoil’s view that such a development would be desirable and important. It is unfortunately not a realistic outcome. We see very few policy signs that would indicate the establishment of a strict, transparent and verifiable global climate agreement before 2020."

And further:

"There is a need to underline the difference between Statoil’s normative approach to climate change, where we support a fast development towards efficient policies and reduced emissions, and our estimation of what is the most likely development. Like any other commercial actor Statoil must base its decisions on our best available knowledge and analysis of current trends; – and these are reflected in our ‘Energy Perspectives’."

Thus, there is a difference between Statoil’s normative approach and the company’s assessment of what is the most likely outcome. The most likely outcome, and the basis for the company’s assessments, emerges in the analysis Energy Perspectives, according to Statoil.

In general terms, it is said that "Statoil complies with climate emission regulations in Norway and in all other countries where it operates. Statoil also supports stricter, more transparent and cost-efficient climate regulations; – in Europe and worldwide. It is part of Statoil’s strategy to be an industry leader in carbon efficiency. The board is concerned that Statoil remains a leading company with regards to CO₂ emissions, and will continue to encourage the Administration to ensure that positive results are achieved in this area.»

However, when the board comments on the proposals that the company should get out of Canadian oil sands and terminate activities in the Arctic, the climate policy is no longer relevant:

«It remains the board’s position that a growing world population and rising standards of living in the developing world will continue to drive energy demand. The areas north of the Arctic Circle are estimated to contain one fifth of the undiscovered, technically recoverable oil and gas resources in the world, and therefore have the potential to be major contributors to the energy supply for decades to come. Access to new exploration acreage, including areas in the Arctic, is fundamental to the company's ambition beyond 2020.»

Both the letter to the think tank Ceres and the response to the critical shareholders were written while Helge Lund was CEO. In Lund’s time, there were no visible signs that Statoil might be reconsidering its strategy in light of stricter climate policies. In an interview in connection with Lund’s resignation, however, chairman of the board Svein Rennemo gave some signals that are worth noting. In talking to the newspaper Stavanger Aftenblad, Rennemo highlighted three challenges the new CEO will have to tackle:

Statoil is not the only oil company having to change its thinking in light of climate policies. Former chief executive of BP, Lord Browne, probably planted some uneasiness in the minds of many chief executives and board members in the petroleum industry in the late autumn of 2014, when he said that many energy and mining companies are ignoring the "existential threat" from climate changes and climate policies and have to change the way they operate.

The message from Lord Browne is that many coal and oil companies are not facing up to the fact that stricter climate policies and increased competition from renewable energy will change the framework for their activities.

The Financial Times quotes from a statement Browne gave at a conference in London in November 2014, where he said that the scientific proof of climate change must be acknowledged. But many in the oil industry refuse to accept this. According to Browne, "this conclusion is not accepted by many in our industry, because they do not want to acknowledge an existential threat to their business".

There is no doubt that Lord Browne’s words were read with interest by powerful people in the oil industry. Statoil’s executive vice president for global strategy, John Knight, tweeted:

"Statoil unequivocally accepts the IPCC’s view regarding climate change. We are not among those Lord Browne criticises".

Statoil is streets ahead of most other oil companies when it comes to accepting climate science. But when it comes to the next step, accepting the consequences of the effects of climate policies for business activities, Statoil, like the rest of the oil industry, is trailing behind. It is interesting to see that an influential actor from the ranks of the industry itself – such as Lord Browne – now agrees with this basic analysis.

According to FT, he used the agreement between US President Obama and China’s Xi as an example. What they have agreed on, cannot be achieved without stricter policies. Together, stricter policies in the US and China could, according to Lord Browne, reduce the two countries’ total oil consumption by over 17 billion barrels over the next 15 years. Then he said, "But many operators remain largely insensitive to the potential consequences of such policies".

According to FT, Lord Browne did not want to be specific about what the oil companies should do, other than that they must accept the climate science and see "the opportunities presented by a low carbon energy system".

Is Statoil’s strategy sustainable in the long-term?

As a company, Statoil is facing fundamental challenges. Cost-saving programmes, divestments and cuts in investment budgets are symptoms of this. The keywords are climate policies and competition from renewable energy as threats to the company’s long-term value creation and growth.

The ethics: Statoil’s spokespersons express, both orally and in writing, great concern over the climate threat, but the company still expects the climate policies to fail. Statoil’s strategic guidelines and investment profile are based on a future energy demand that far exceeds what the climate will be able to handle.

Those who have the authority to represent Statoil in connection with climate and energy issues in public, for instance chief economist Eirik Wærness and senior vice president for climate issues, Hege Norheim, give the impression that Statoil bases its activities on the UN’s agreed two-degree target. But Statoil does not believe in the two-degree target. Statoil believes that the world’s energy consumption will develop along lines that far exceed what science tells us the climate can handle. This is communicated in the analysis Energy Perspectives and in reports to the AGM, as the first part of this memo shows. The reason why the company is going for both oil sands in Canada and activities in the Arctic, is continued growth in oil demand far into the future. Statoil is not alone: Shell and Exxon agree. But where are the ethics in an attitude like this?

There is no reason to doubt that Statoil’s top management is deeply worried about the risks related to climate change. But the company cannot forever communicate opposing views, where verbal concerns go in one direction, while strategic guidelines and cash flows go in the opposite direction. They aren’t practicing what they preach.

The politics: In the past, Statoil’s answer to each and every issue related to climate policy has been that a global price for CO₂ emissions is required. That is the solution meant to fix everything. This approach seems to show that the company takes the climate problem seriously, but it is also an answer that relieves the company of responsibility and places that responsibility on the shoulders of politicians.

A global, and sufficiently high, CO₂ price would have its advantages. But there is nothing to indicate that we will ever see a global climate regime of the type Statoil wants – and hence an equal CO₂ price. A global CO₂ price presupposes a binding agreement with an emissions ceiling everyone is committed to.

If anything is certain ahead of the climate summit in Paris this autumn, it is that we will not achieve an agreement in line with such a model. There will be no global emissions ceiling leading to a global carbon price.

The political reality Statoil and other energy companies are forced to engage with, is a patchwork of political instruments and regimes, rather untidy and with low predictability. At the same time, wide-ranging technological changes are taking place that make renewable energy more competitive compared with coal, oil and gas.

Based on both ethical and political considerations, Statoil’s board and management must ask how they can act responsibly and do the right thing in a world where climate policies are successful – but without an agreement that results in a global carbon price.

The strategy: There is growing concern in financial circles over the oil companies’ neglect of the risks associated with future energy demand in light of stricter climate policies and cheaper renewable energy. Which projects will be unprofitable in a world where oil consumption levels out and drops? For Statoil, efforts in the Arctic are particularly under threat. This is the story of the carbon bubble.

The oil price drop has contributed significantly to this uncertainty and will most certainly lead to a number of expensive petroleum projects being postponed or even abandoned. The Oslo-based consultancy Rystad Energy has calculated that investments for a dizzying USD 150 billion will be put aside in 2015 in relation to plans announced earlier. From a climate point of view, this is positive. The carbon bubble risk will be lessened, and investments will go to sectors where they will do more good.

An oil company such as Statoil needs a much higher oil price than the current USD 50-60 per barrel to be able to justify both dividends and the current investment level.

No-one knows whether the oil price will again reach its former peaks. The drop in the past six months is primarily supply-driven – American shale oil can be recovered in large volumes and therefore lessens the need for more expensive oil. At the same time, there are strong trends in the direction of lower demand growth.

Of course, the current low prices may lead to such strong reductions in investments that a new price boom will follow in a few years’ time. But here, climate policies and energy restructuring will play an important role. For instance, in a very positive trend throughout the autumn months of 2014, a number of countries, e.g. India, Indonesia and Kuwait, have been cutting subsidies in line with the oil price drop. It is virtually only in the US that lower oil prices affect market prices directly. Elsewhere in the world, oil is mostly subsidised or taxed. The effect at the petrol pump is not as dramatic as the changes in the producer prices.

Helge Lund was not keen to talk about Statoil or his new job with the BG Group when he was interviewed in the beginning of January 2015. But he believes the oil price will rise again, and that we should be looking at the "fundamental factors over time. You have to look at the long-term marginal cost of generating new production. That is what will determine the price picture over time,"Lund said.

If the climate policies are successful, oil demand will be far lower in a couple of decades than if the climate policies fail. This will affect the price. According to the IEA, in a two-degree scenario, oil demand in 2040 will be about 30 million barrels per day lower than in the new policy scenario – a scenario in line with Statoil’s own view of the future.

This graph, from the Climate Policy Initiative, shows how the oil companies will suffer a "double loss" if demand drops.

Reduced oil consumption means that producers will lose on two fronts. The most expensive projects will not be needed and will therefore not be developed. But even more important is the loss of value for the rest of the production, because lower prices lead to far lower margins on the cheapest projects.

This raises some difficult questions:

Let us try a different line of thought: Society doesn’t actually require the products Statoil delivers, i.e. oil and gas. What society actually requires is energy services: cars that run, warm houses, lighting.

For a couple of hundred years, coal, oil and gas have been the most important raw materials in the production of energy services. Fossil energy sources have provided the world with light and heating and made it possible to transport people and goods in cars, on ships and by aeroplane.

But what happens when energy services can be produced and supplied cheaper and more efficiently – and with fewer harmful effects to the environment, life and health – in ways other than burning coal, oil and gas? The climate policy and rapid technological development, coupled with the cost increase in the recovery of fossil energy, means there can only be one end to this story.

How fast this might happen is uncertain, but there is no doubt about the direction in which things are moving.

It is of course correct that in the decades to come, there will also be a significant need for oil and gas, but the question is how much will be required. Will the market demand the most expensive oil and gas – such as oil and gas from the Arctic – or will we manage without it?

It is indubitably necessary for Statoil to cut costs. But how is the company to achieve new growth following the cost cuts?

A company that deals exclusively with upstream oil and gas hardly has a sustainable business model in the long run, in the light of climate change and increased competition from renewable energy. Statoil’s activity is related to large stand-alone projects with long lifetimes. Therefore, the company is vulnerable with regard to both cash flow and risk connected to market changes. Changed circumstances, such as cheap solar energy and strengthened climate policies, represent a significant threat. These are conditions the company can do little to change.

This description of reality should not in fact be considered controversial. But different stakeholders will have different interests when it comes to the company’s strategic choices moving forward.

Statoil’s private shareholders have more reason to take an interest in stock market prices than the government has. Measures that strengthen share prices in the short-term – such as cost-saving programmes and investment cuts – will therefore be applauded by the stock market. The state has a virtual eternity perspective on its ownership, and short-term fluctuations in the stock market are therefore of less importance. Not even Norway’s present right-wing cabinet seems interested in selling off Statoil shares.

Last summer, Professor Klaus Mohn wrote in his column on Norwegian news site Sysla that the state should leave Statoil at the same rate as Statoil is leaving the state. The development of international activities makes the Norwegian part of Statoil less important, and according to Mohn, this is an argument in support of the state selling off shares.

It is not difficult to follow Klaus Mohn here. Of course it does not make sense for the Norwegian state to own two-thirds of a company that is investing heavily in expansion at the high risk end of the global petroleum industry.

Statoil has cultivated its role as a "technological upstream company" – that means exploration in every tricky nook and cranny on the planet; Nicaragua, Russia, Colombia. Coupled with their efforts in the Arctic, a more or less successful operation in the US, and the Canadian oil sands to hold them back, one would have to search long and hard to find arguments against the state divesting of shares.

From the point of view of employees and trade unions, the most important argument will be related to how Statoil can best secure jobs both internally in the company and in all the activities where Statoil is a customer in one way or another. Strong efforts internationally have undoubtedly meant a positive knock-on effect for the Norwegian supplier industry, but strength in the global petroleum industry is only a hedge to the degree a downturn in the Norwegian oil sector is not accompanied by a corresponding downturn internationally. A downturn in the Norwegian oil sector which is due to a depletion of resources on the Norwegian Continental Shelf, is different from a general downturn in the global oil industry where expensive projects are abandoned from pole to pole. The latter is what we now see playing out.

From the point of view of the state, purely financial arguments could speak in favour of harvesting, i.e. that the company empties the Norwegian Continental Shelf under high tax pressure, while high dividends are taken and as little as possible is reinvested. In this way, Statoil could bring in plenty of money for the state, but not be a company that grows.

For the employees – and the company management – this is not an attractive strategy. It is no fun being sentenced to a slow death, with new cost reductions and job cuts year after year. It is more fun to grow, and most fun when the growth is profitable. Then both employees and shareholders are happy.

So the question is: Can Statoil grow profitably without expanding into things other than recovery of oil and gas?

In a scenario where demand for the company’s products gradually weakens and prices stay low, the answer is probably no. If the answer is to be yes, Statoil has to be significantly better and more cost effective than all its competitors and win significant shares in a falling market.

In a scenario where demand for oil and gas continues to increase and prices also gradually follow the upward trend, the picture is of course different. But then we are looking at a world where climate policies are failing virtually across the board.

Statoil in renewable energy – a political "duty"

In 2009, Statoil changed its mission statement so that not only oil and gas, but also "other forms of energy" became part of the company’s activities. This was in Terje Riis-Johansen’s time as Minister of Petroleum and Energy, and he wanted Statoil to demonstrate its commitment to renewable energy.

This was about the same time as Statoil was setting up the floating Hywind wind turbine outside Karmøy in West Norway. The company also had some land-based wind projects that were later sold. Statoil highlighted offshore wind power as the part of the renewable energy sector where it had a comparative advantage, and it has in partnership with Statkraft built a couple of offshore wind farms in the UK. But nothing in Statoil’s communication with the outside world indicates that the efforts made in offshore wind power were considered to be of strategic importance. The impression that was created in Helge Lund’s time was that this was something not done out of genuine interest, but out of political "duty".

An interview in newspaper Stavanger Aftenblad in 2010 stated that "CEO Helge Lund will test out the green paint for another three to four years before he decides whether the oil company will continue to pursue offshore wind and other types of new renewable energy."

"99.5 per cent of Statoil’s activities are connected to oil and gas. If fossil fuels continue to dominate the global energy picture over the next few decades, within three to four years we will have to consider whether it is right to focus on renewable energy as well as on oil and gas," says CEO of Statoil Helge Lund.

He is of the opinion that one of the most important tasks moving forward is bringing the costs of renewable energy down.

"The question is whether we are the right people to be taking on these challenges, or whether we should be cultivating the role of oil and gas company and pour all our efforts into the cleanest possible production, and carbon capture and storage (CCS)", says Lund.

Stavanger Aftenblad describes Lund as straightforward and decent, charming and capable, a scout leader who has grown up.

"But sometimes things get heated. For instance when he is criticised for not being interested enough in renewable energy", writes Stavanger Aftenblad. Then, Helge Lund is quoted thus: "Many people want Statoil to invest in all sorts of new renewable energy, often regardless of any realistic chance of making a profit within a reasonable time frame. This is an easy stance to take for anyone not required to generate profits. But I know who will get the blame if Statoil invests NOK five billion in something that is popular today, but a failure in five years," Lund says, firmly.

Almost five years after this interview was printed, there is reason to ask whether Helge Lund thought of renewable energy as some sort of passing fad. But the issue he highlights is a real one. Is it right of Statoil to continue to pursue renewable energy somewhat half-heartedly? Should the company pull out, or redouble their efforts?

What may be the most important shift in the energy sector throughout the almost five years that have passed since Helge Lund gave this interview, is the price drop for solar energy. Those loyal to oil and gas will probably claim that shale oil represents a more important development; but the growth in solar energy likely represents a more fundamental shift.

Like the rest of the fossil energy sector, Statoil overlooked how solar energy was starting to emerge as a viable alternative. For instance, in 2012 McKinsey presented analyses that concluded that the price drop we have seen in recent years can only be expected to continue. It is not about mystical solutions that will solve everything in the blink of an eye, but gradual improvements that are partly due to research-based progress, and partly to the market maturing. It is about continuous improvement; cost reductions throughout the value chain.

Instead of listening to McKinsey, Statoil leaned towards IEA’s presentations of the macro picture in the energy field, which indicate that a fundamental change in the energy sector is not taking place. In its executive summaries, the IEA provides a superficial snapshot which borders on patronising. One has to dig down deep – into quite nerdy details – in order to see what is happening. The IEA has fundamentally underestimated the rate of growth in wind and solar energy, and the institution’s "new policies scenario" which is presented in Norway every autumn under the auspices of Statoil, shows that solar and wind power will continue to be only marginal sources of energy.

Just how far off IEA has been in its assessments of solar energy, has been documented by e.g. Terje Osmundsen in the report "IEA and solar PV: two worlds apart".

The future is renewable. But it is also decentralised. The green shift is characterised by energy solutions developed on a smaller scale. New technologies and combinations of technologies – for instance solar power and batteries – are changing the energy markets. Each investment is not that large, and projects can be realised swiftly. For this reason, big changes can happen rapidly – when many players do the same thing at the same time.

The falling prices of solar energy (PV) have in just a few years made solar competitive in a large number of markets. But we have only seen the beginning. When solar power can compete with the price people are paying for electricity from the grid, the stage will be set for quick changes.

Solar energy is revolutionary because it kills off old monopolies and semi-monopolies. Everyone can produce their own power. Solar energy disturbs price formation in the power markets. The German energy giants’ fate is to a large degree owed to the breakthrough of solar energy. Decentralised power generation has changed the framework for how the energy system operates, just like the internet has turned most things in the media and entertainment business upside-down in the last two decades.

E.ON’s decision in the autumn of 2014 to split the company, in rough terms into a renewable part and a fossil part, is a powerful illustration of this development.

The power sector is moving from a sort of "Soviet model" where large, centralised units with one way distribution are supplemented, and possibly taken over, by a system more similar to the internet; a number of small interconnected units that both generate and consume. Like the traditional power sector, the petroleum industry is very long-term and built up around large, centralised units. The exception in the oil sector is shale oil, where lead times are much shorter and myriad players take part.

A new business model

Statoil operates in a part of the energy sector that is very long-term. The strategy has been fine-tuned for focusing on upstream oil and gas, often in demanding and inhospitable areas, whether this is in the Arctic or in politically difficult regions. The common denominator is that it takes a very long time for a project to make it all the way from an initial green light to actual profits. Lead times are long.

To the degree Statoil has taken up a position in renewable energy, it is in offshore wind power. Offshore wind power is characterised by the same thing as the company’s other activities where lead times and the size of individual projects are concerned: large individual investments with long planning horizons are the order of the day.

The company has no position in the renewable and decentralised spheres and will therefore be vulnerable to a green shift.

Statoil can compensate for this risk by growing in the renewable part of the energy sector, but this presupposes that it redefines itself as a company that delivers energy services. You have to dare to bite your own tail, eat yourself, rather than be eaten by others – as Kjell Aamot, President and CEO of the Schibsted media company said when it let a focus on digital newspapers erode the income basis of their printed newspapers.

Statoil’s board and management should ask themselves whether the company is correctly positioned in terms of strategy, or whether it should focus on developing business areas that are both low carbon/renewable and decentralised.

The business idea for a restructured Statoil will no longer be to pump oil and gas, but to supply society with energy services it needs and is asking for. Statoil can become a large player in renewable energy. Development and construction of hybrid power stations combining solar, wind and gas power – or solar, wind and diesel power in developing countries – is a good example. Hybrid power stations can deliver the same volume of power using significantly less gas or diesel. The greater the renewable component, the less CO₂. The power will also be cheaper.

This would be a long-term sustainable business model which also allows for oil and gas production, but where this is not the ultimate goal of the activities. The goal will be to deliver energy services people need, which bring the world forward, and which are compatible with a two-degree target.

Financially, the upside will be that the road is much shorter from investment to cash flow than in upstream oil and gas. Large solar power stations can be planned and built in the space of a few months. Supplementary gas power plants also have fairly short construction times. These are markets in growth. It will happen whether the oil industry likes it or not.

Summary

It is not easy being an oil company with the climate threat hanging over us. Much oil and gas will be needed for a long time to come, even in a world dealing with the climate challenge. But far less fossil energy will be required in a world that succeeds than in a world that fails. An oil company with a future must therefore ask: Is our current business model helping to make the world a better place? How can we help the climate policy succeed – and at the same time make money on the restructuring?